Lorem ipsum dolor sit amet, consectetur adipiscing elit.

Date : 15-jun-2020

Choose how you'd like to connect with us

News Details

Update Date : 13-Dec-2024

Created Date : 10-Jun-2022

Reference : Money Control

The central government on Friday ratified the interest rate of 8.1 percent on employees’ provident fund (EPF) contributions for the financial year 2021-22.

In March, the Employees' Provident Fund Organisation (EPFO) declared this rate — the lowest in four decades, much to the disappointment of many. The next step will be to initiate the process of crediting the interest into their accounts.

EPF’S TAXABILITY RULES

For salaried employees with hefty pay packages, it’s a double whammy of sorts. In Budget 2021, Finance Minister Nirmala Sitharaman decided to tax interest earned on annual Employees’ Provident Fund contributions in excess of Rs 2.5 lakh (Rs 5 lakh for government employees), taking taxpayers expecting sops during a COVID-19-hit year by surprise. Until then, EPF was completely tax-free at all stages: investment, accumulation and maturity.

While the announcement was made over a year ago, such employees will feel the pinch when the EPFO credits the 8.1 percent interest to members’ accounts. That is, the retirement body will deduct tax (TDS) at the rate of 10 percent at the time of crediting interest for the financial year 2021-22. “TDS will also be applicable in the case of provident fund final settlement, transfer claims, past accumulations transfer, on transfer from exempted establishments to EPFO and vice-versa, at time of annual accounts processing...death cases…,” the EPFO circular said.

Apart from high-earners, those who contribute to their voluntary provident fund (VPF) beyond this limit are also bound to be affected.

Read on to understand the nitty-gritty of how your EPF statements will look this year.

WHAT IS A NON-TAXABLE ACCOUNT?

As per a Central Board of Direct Taxes (CBDT) circular, your EPF statement will be divided into two parts: taxable and non-taxable accounts. This is of significance if your annual EPF/VPF contribution exceeds Rs 2.5 lakh. For others, it's business as usual as the interest on their contributions will not fall in the tax net. The new format will come into effect from April 1, 2022, for the last financial year (2021-22), the EPFO had said in its April circular. The non-taxable component of your statement will reflect the closing balance in your EPF account as of March 31, 2021, non-taxable contributions (lower than Rs 2.5 lakh) made during the year, interest earned on this component and so on.

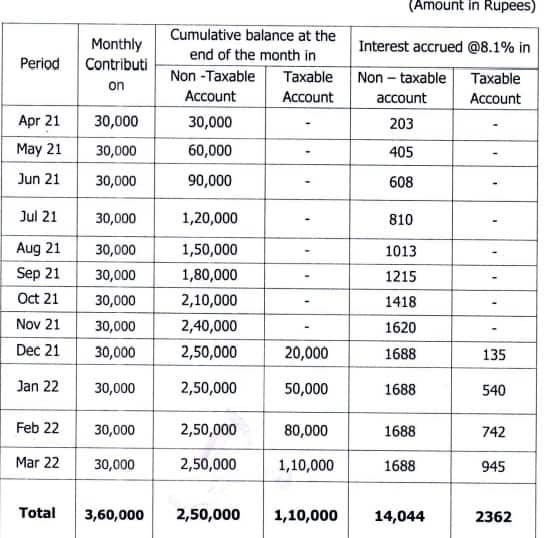

Interest is credited on an annual basis, but employees’ PF accounts are maintained on a monthly basis. So, the segregation between taxable and non-taxable contributions and applicable interest will be done on a monthly basis. Let’s take the illustration that EPFO has provided in its circular (see table below). If your share in PF contribution as an employee is Rs 30,000 every month, you would have breached the Rs 2.5 lakh threshold for 2021-22 only in December 2021. So, up to November 2021, your contribution and the interest earned on this amount until then will be displayed on the ‘non-taxable’ side of the statement. “The process is fairly simple. And, the non-taxable and taxable bifurcation will happen at the EPFO’s end. So, employees or employers need not be worried about ensuring that the segregation is accurate,” says Sudhir Kaushik, Co-founder of TaxSpanner.com, a tax consultancy firm.

HOW WILL THE TAXABLE ACCOUNT WORK?

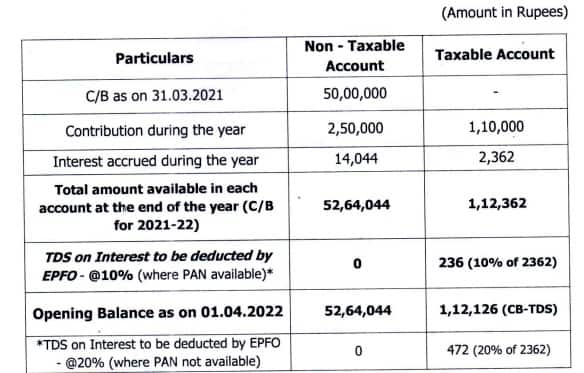

The moment this contribution crosses the Rs 2.5-lakh mark, the excess contribution every month and applicable interest will shift to the taxable account. And, interest earned on this component will attract tax. The EPFO will deduct tax at the rate of 10 percent before crediting the interest if you have furnished your PAN. If you haven’t, the tax will be deducted at double the rate (see illustration provided by EPFO below).

HOW WILL WITHDRAWALS BE ACCOUNTED FOR? WHAT WILL BE THE TAX IMPLICATIONS?

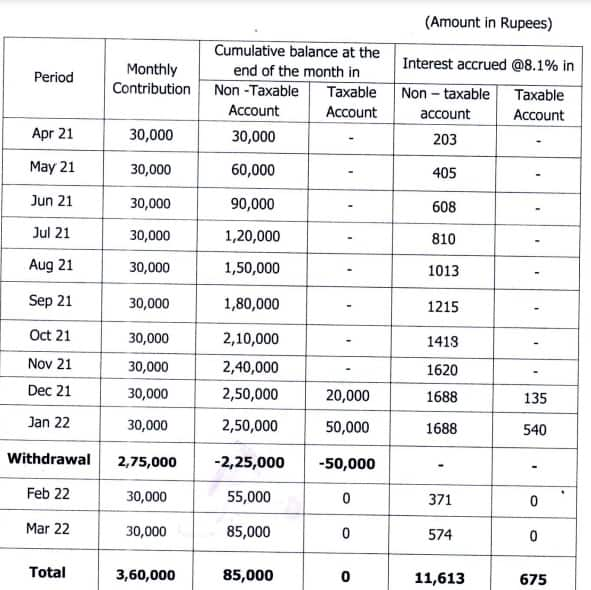

Let’s say an employee contributing Rs 30,000 per month decides to make a withdrawal of Rs 2.75 lakh at the end of January. Therefore, until then she would have contributed a total of Rs 3 lakh (see EPFO’s table below). In such a case, the deduction will be first effected in the taxable account, so as to ensure that the tax impact is lighter for employees. “So, the withdrawal would first be made from the taxable account, and only after that is exhausted will the non-taxable account be tapped,” says Preeti Chandrashekhar, India Business Leader, Health and Wealth, Mercer India. So, in the illustration below, taxable and non-taxable accounts have balances of Rs 50,000 and Rs 2,50,000, respectively, in January. “So, if you withdraw Rs 2,75,000, it would first get deducted from the taxable account that has only Rs 50,000 as balance. The remaining Rs 2.25 lakh will be withdrawn from the non-taxable account,” she explains.

SO, IT’S THE EPFO’S RESPONSIBILITY TO SPLIT MY CONTRIBUTION INTO TAXABLE AND NON-TAXABLE COMPONENTS AND DEDUCT TAX. WILL I HAVE TO TAKE ANY ACTION ON MY END WHILE FILING MY INCOME TAX RETURNS?

Yes, you will have to be mindful of an additional task that you have to complete at the time of filing returns. “The EPFO will withhold TDS at the rate of 10 percent. However, you will have to calculate the total tax payable on the basis of the tax bracket you fall into. It is likely that you will have to pay additional tax on this amount at the time of filing returns,” says Prableen Bajpai, Founder of Finfix Research and Analytics. The process will be similar to how interest earned on bank fixed deposits, for example, which fall under ‘Income from other sources' is taxed. “You will have to pay tax on an accrued basis, as per the slab rate applicable to you. Since the EPFO will withhold TDS, it will be reflected in the annual information statement and will also be pre-populated in the income tax return forms. Not paying taxes at the time of filing returns could lead to queries from the income tax department,” says chartered accountant Karan Batra, Founder, Chartered Club. For those who have not furnished their permanent account number (PAN), the TDS rate will be much higher at 20 percent. For non-resident employees, the TDS rate will be 30 percent.

Date : 15-jun-2020

Date : 15-jun-2020

Date : 15-jun-2020

Date : 15-jun-2020

Leave a Reply

You must Login for Leave a Reply.

Comments (0)